Health Insurance startups enter the digital health market

Health Insurance system: A brief overview

Health insurance is a protection that the insured person buys to cover himself against the cost of medical expenses like medicines, surgery and hospitalisation. Depending on the insurance cover opted for, some or all illnesses, critical illnesses and surgical processes could be covered by that insurance. As per a WHO report of 2015, as many 400 million people did not have adequate health insurance coverage, which was a worrying 6% of the world population in 2015. Let us see what percentage of people at three different age groups fared concerning health insurance coverage in the United States of America.

| Type of Insurance | > 65 years old | < 18 years old | Between 18 – 64 |

|---|---|---|---|

| Uninsured | 10 | 5 | 12 |

| Privately Insured | 65 | 53 | 69 |

| Public Insurance | 25 | 42 | 19 |

Source: CDC Gov

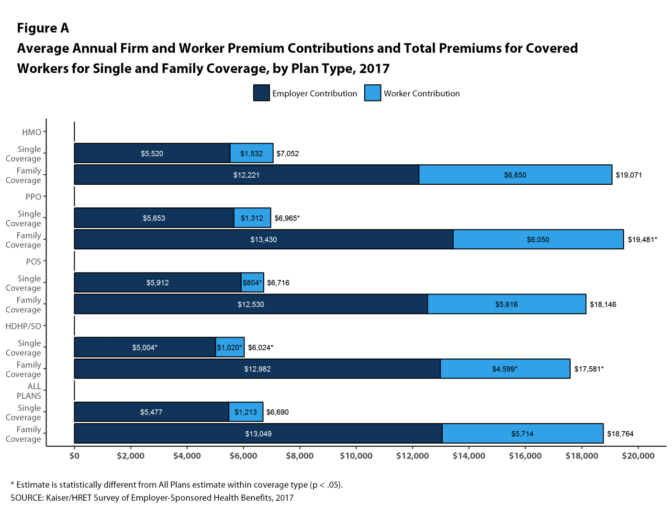

As we can see above, a significant part of health coverage was through private health insurance covers taken by individuals or by employers. This is in spite of the fact that health insurance offered by private insurers is becoming increasingly expensive every year. There are several reasons for this. A significant chunk of the insurance premiums charged by private health insurers goes towards non-medical expenses like administrative costs and promotional costs. Even under medical expenses, most private health policies include at least one annual checkup or doctor consultation, also if the insured person doesn’t have any major surgery or illness. To quote a few examples, the average health insurance premium for 2017 in the USA for employees covered by employers was almost $19000 per annum, of which employees themselves contributed nearly a third.

Image courtesy of NCSL

Another example from Germany, which has one of the world’s best healthcare systems, shows us that the comparatively cheaper government covered health insurance is almost $1000 (or 800 Euros) per annum, of which half is to be paid by the insured person. If someone opts for private insurance, the premium would be at least 4 to 5 times higher.

Startups in the health insurance space can fill in the real gaps outlined above.

Because of the high penetration of smartphone technology in every country today, health insurance startups would find it easier to touch more people who do not have coverage.

Also, by better use of data, the number of hospitals and doctors could come down drastically. With administration costs already very low for startups, the overall cost of providing health insurance would come down.

The idea behind Health Insurance startups

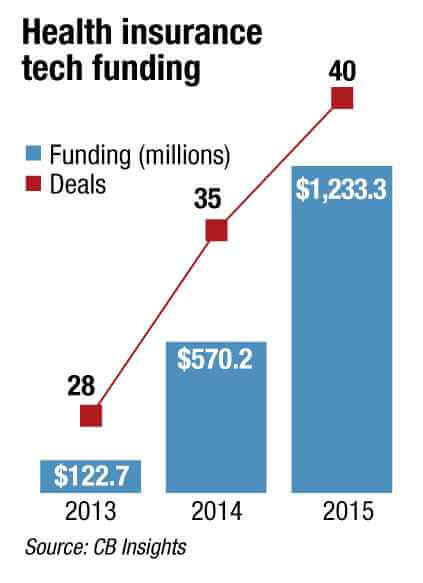

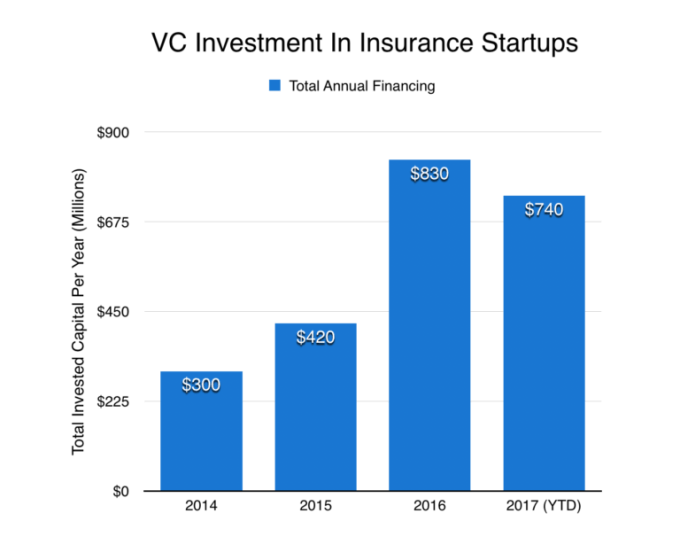

Startups have been started for almost every aspect of human endeavour. But the interest of startups towards insurance in general, and health insurance, in particular, has been slow. It is only now that investors and startups have begun to see the immense potential in health insurance. The chart below shows the exponential explosion in the number of funding deals in healthcare startups and also the amount of funding in recent years.

Image courtesy of Modern Healthcare

Some startups address the problem of reach, some specialise in data and the dynamic analysis of health data, whereas some startups take up complete health coverage in partnership with a traditional health insurer. What makes any startup different is that the way they do business would bring down the costs of coverage, and that reduction can be passed on to the person taking insurance.

But apart from lower prices and easy access, the essential benefit that startups are offering is the use of technology to make health insurance more efficient and easy to use. The insured person can get real-time tracking of his or her health condition using just a smartphone application. Correct and regular use of the fitness trackers can also help a person lower his or her insurance premiums.

Instead of going through long lists of doctors whom they can consult, the startup can provide them with a list of correct doctors in their vicinity who usually treat the ailments they are suffering from. The consultation with that doctor can even take place through video chat sitting in the comfort of their home, which would be a big bonus for a person who is aged or disabled and for whom it is not convenient to travel long distances to visit the doctor. The app or website could also provide the details of visiting hours for the doctors.

Even when one needs to file a claim on a health insurance policy, it would be a simple matter of a few clicks and swipes on the app, as opposed to multiple visits and countless forms in the case of traditional insurers. Tissue Analytics (wound treatment), AliveCor (cardio), NetraLabs (Eyes) are just a few examples of startups exploiting cutting-edge technology.

Apart from these digital health technologies, the startups operating in the health insurance space are also using non-medical technology like Artificial Intelligence (AI), Internet of Things (IoT), Blockchain etc., and even harnessing the power of social media.

| Recommended for you | |

| 108 Health Insurance companies, brokers in India | |

| Statutory Health Insurance in Germany | |

| How empowered patients and digital prevention improve healthcare? |

Latest players in the Health Insurance industry

The real extent of venture capital funding into health insurance startups is not very clear, because different startups are into various parts of health insurance, unlike the full risk providing traditional insurance companies. The chart below shows the steady growth in funding (with 2017 data only available for the first nine months).

Image courtesy of Techcrunch

A large number of health insurance startups are making their presence felt across the world. Some of those big names are Clover Health, Maxwell Health, Ottonova, Zenefits, Affordplan, Medigo and Grant4Apps, although there is a vast number other than these names.

Clover Health provides several additional benefits to clients in the US which regular Medicare does not. For example, they give incentives to patients to stay healthy; they also offer routine hearing care, dental care, and vision care.

Affordplan is positioning itself as a mix of a financial services startup and a health insurance startup. They allow clients to choose the specific treatment or ailment they wish to prepare for and then encouraging them to deposit appropriate amounts on a regular basis and build up a kitty so that they are financially made when they need coverage. It is neither a loan nor an insurance policy but serves the purpose of both.

What is the future of Health Insurance startups?

To summarise, the burgeoning costs of private health insurance provided by traditional insurers paved the way and created the space for health insurance startups to disrupt the health insurance space. The cost-effectiveness, ease of use and better care due to the use of technology – these are some of the primary reasons why startups in health insurance are increasingly displacing traditional health insurance providers.

These new age startups can ensure that affordable and efficient health insurance is within easy reach of everyone on the planet, even if they do not enjoy any government health coverage.

As more and more incisive technology is used in the architecture of health insurance models, the health insurance startups can quickly do what the traditional companies have not been able to – provide easy to use ways of keeping healthy, reducing health insurance premiums, complete hospital and doctor visits readily (and remotely if needed), and file claims effortlessly.

That is where the immense potential for healthcare startups lies.

Image credit: www.istockphoto.com